You're not stuck, you're just alone at the top. Most entrepreneurs hit a ceiling, not because the opportunity isn't there, but because you're solving $10M problems with $1M strategies.

Would you buy this $1.6M kitchen redesign business?

June 25, 2025

8 min read

👋 Welcome to The Main Street Minute, your shortcut to Main Street acquisitions.

This week, we take you inside a promising deal: experienced operator, growing biz, legacy-focused sellers. What could go wrong? Everything, it turns out. But not for the reasons you'd expect. Let's dive in…

THE SETUP

First-Timer Buyer Eager for Feedback

Not too long ago, Kurt came to Monday Night Live knowing exactly what he needed:

To get grilled.

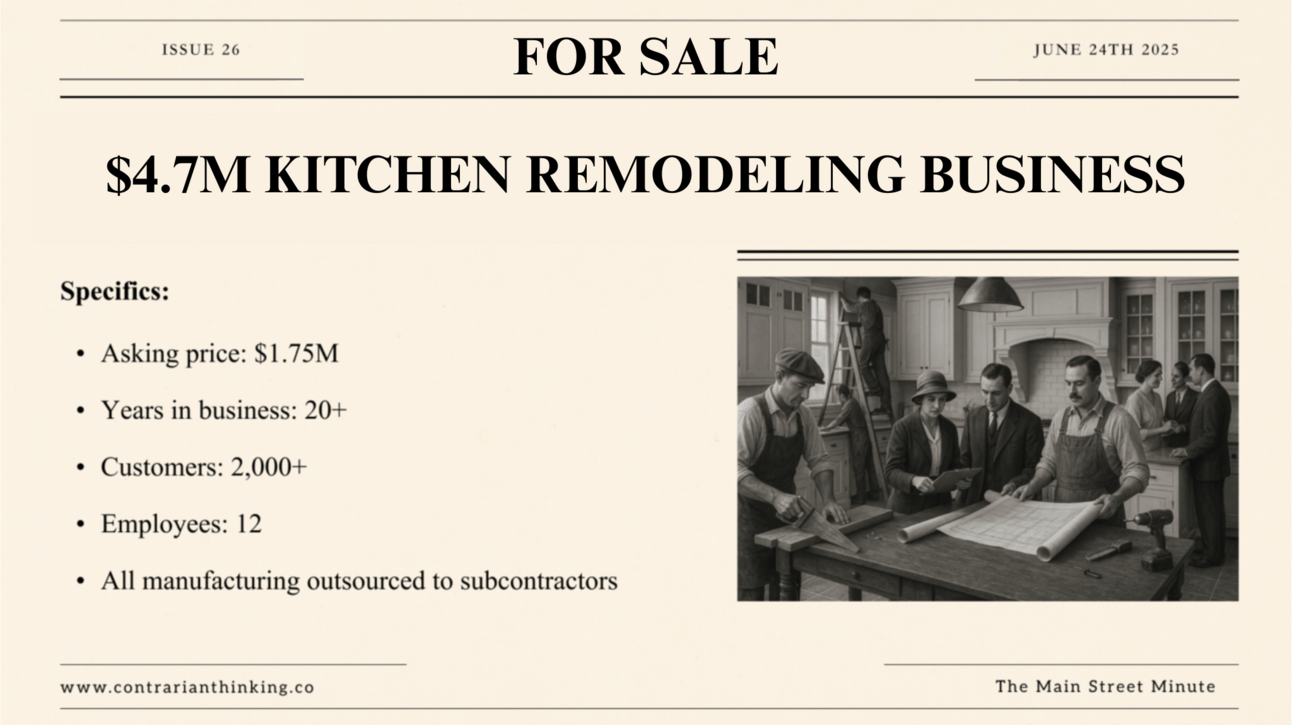

Three months in the Contrarian Community, he'd been stalking this Arizona kitchen design business for weeks. Already signed the NDA. Already met the sellers. Revenue climbing 10% year-over-year to $4.7M.

His plan seemed solid:

Pay $1.5M-$1.6M (down from $1.75M asking price)

Keep the design "superstar" who runs sales

Use his manufacturing experience to optimize operations

The sellers even said the magic words:

"Legacy and people matter more than price."

But then, our buying coach Hants started asking questions, and delivered exactly the heat Kurt had asked for.

THE BUSINESS

Legacy Kitchen Company at a Crossroads

This Arizona kitchen design biz was family-owned and growing, but in transition. Half the 12-person staff was hired in the past year.

The Business Model:

High-end kitchen design and construction

In-house design, outsourced manufacturing

Established showroom and homebuilder partnerships

50% deposits upfront

Premium pricing in Arizona's booming residential market

On paper, this kitchen design company had solid fundamentals:

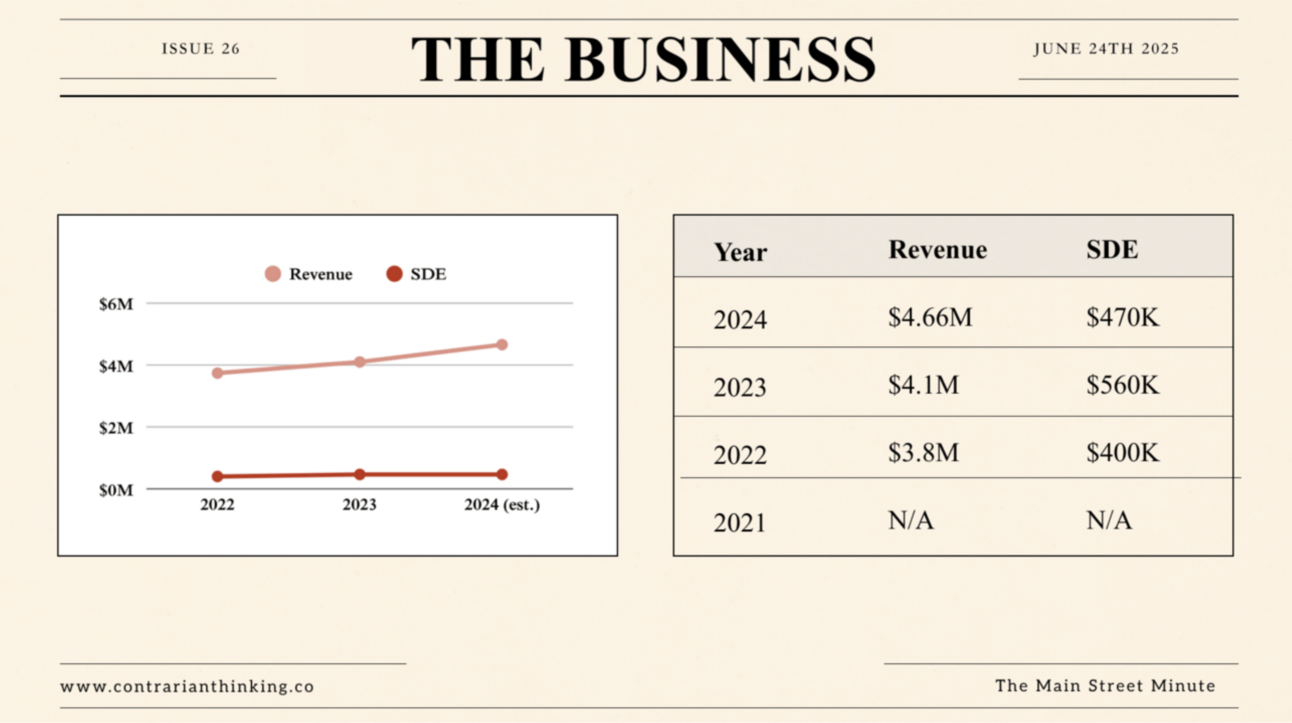

The Numbers:

Revenue: Steady ~10% YoY growth

SDE: $470k (SDE = Seller's Discretionary Earnings, the cash a business generates for its owner)

Assets: $470k in equipment and showroom

Healthy profit margins at 9.9% (slightly above industry standard)

Even better: One key owner (the design manager) was staying on. Kurt called her a "superstar" who'd be "difficult to replace."

So what was the problem?

THE RED FLAGS

Veteran Consultant Cuts Through the Hype

Hants White, a community facilitator with 25+ years of business consulting experience, immediately started probing Kurt’s assumptions.

Problem #1: Cutting Employee Pay to Fix Deal Math Was An Illusion

Kurt wanted to cut the superstar's $75k salary in half, hope she'd make it up in commissions, and use the "savings" to make his spreadsheet look better. He didn’t include the expected performance-based salary. Hants didn't let that slide:

Problem #2: The SBA Rules May Strip Away The Business’s Contractor License Upon Owner Transition

This is a construction business. Kurt doesn’t have a license. And new SBA rules mean he may not qualify to inherit the existing one. Big red flag.

Problem #3: The Debt Service Danger

At 1.39x coverage (meaning the business generates $1.39 for every $1 of loan payments), there wasn't much cushion for problems.

And then came the valuation talk...

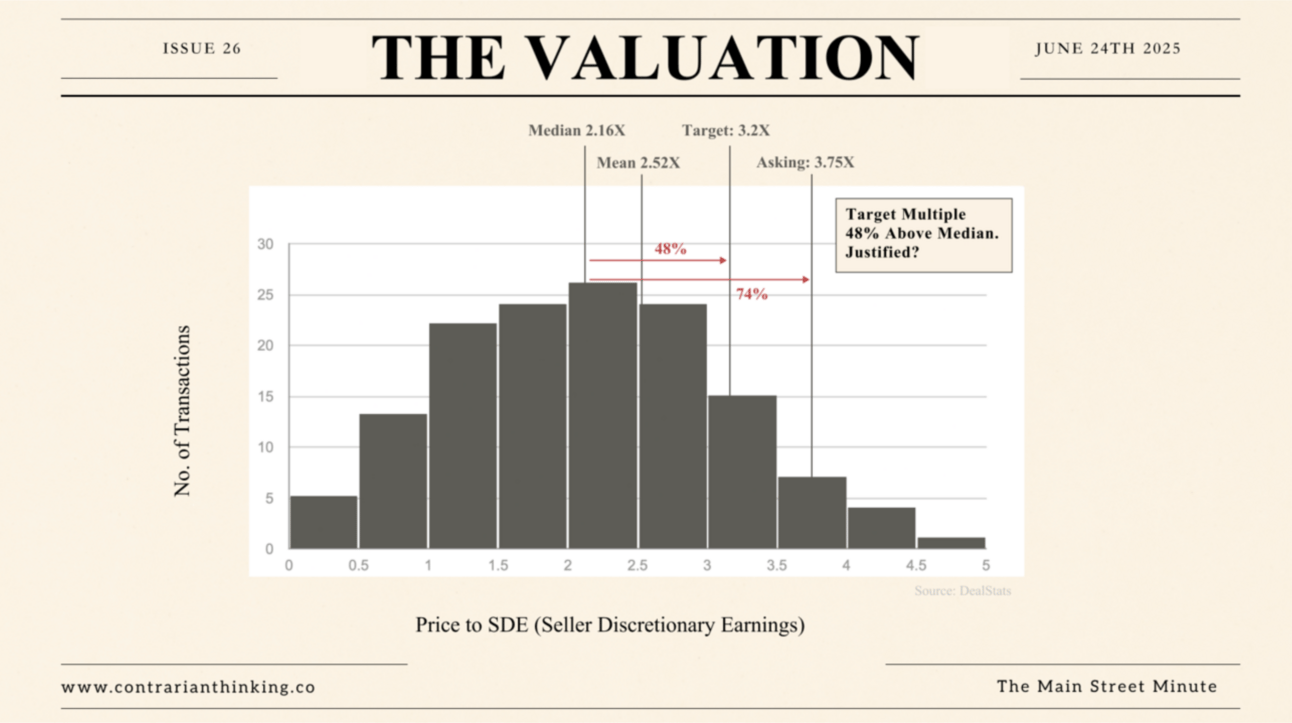

WHAT’S IT WORTH?

Measuring Kurt’s Deal Against Market Data

While Kurt was getting grilled on operations, the valuation picture was becoming clearer.

Now, if you only look at the 74%-above-median multiple, the valuation may sound high.

But as we teach in the Contrarian Community, never look at multiples in isolation.

This business employs 12 people and generates $4.7M annually. According to market data, average residential remodeling businesses employ 3 workers and generate $1M annually. Larger companies almost always command higher multiples.

Even at his target $1.5M price (3.2x SDE), Kurt would still be paying above industry norms — but for a business significantly larger and more established than typical players.

This might explain why the debt service coverage was so tight...

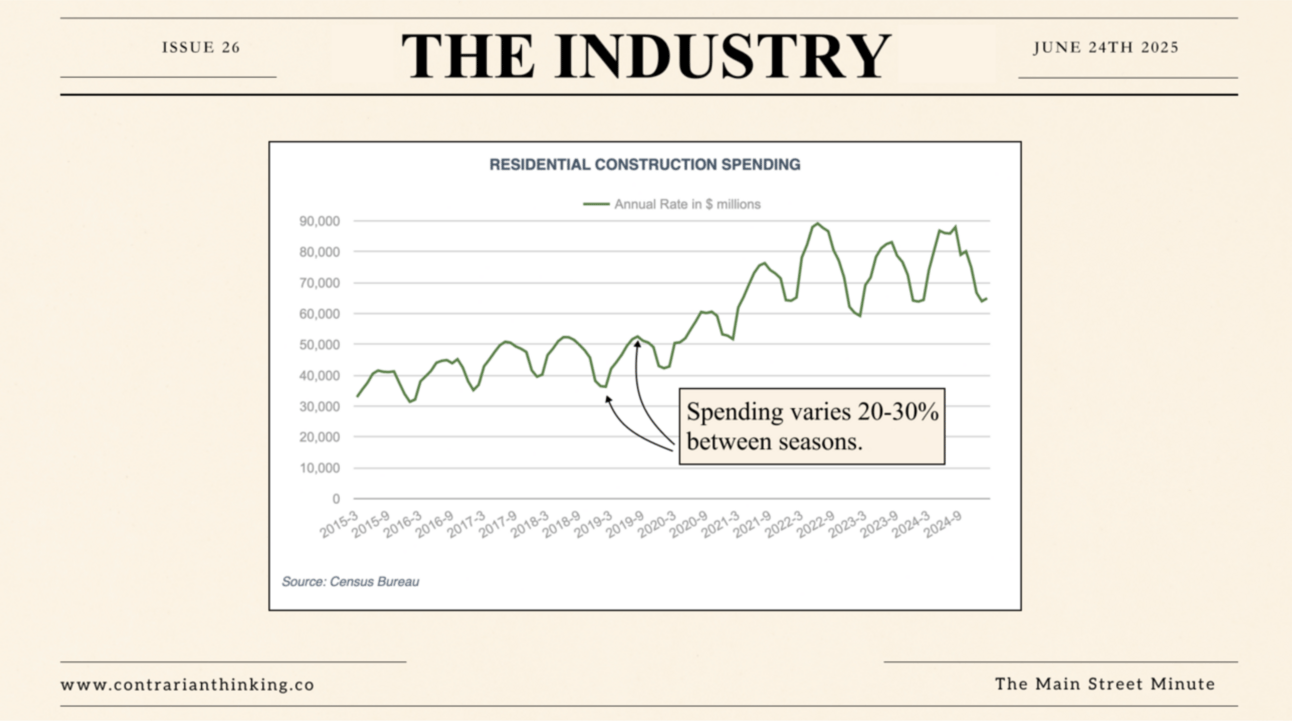

The residential remodeling industry is a $142.9B market, but it has some sobering realities:

14% business exit rate (vs. 9.5% all industries)

Revenue fell 25% during the 2007-2009 recession

SBA charge-off rate: 8.33% (vs 4.26% all industries), meaning loans in this industry default more often

Construction spending swings wildly throughout the year, creating cash flow nightmares.

At Kurt’s proposed 1.39x debt service coverage ratio, a 25% revenue drop (like what happened during the 2007-2009 recession) would push his coverage dangerously close to 1.0x — the territory where businesses start defaulting on loans.

Kurt had plugged in $100k as "salary needed" because he was leaving his W-2 job and wanted that salary. But did he need all of it?

Probably not, he admitted.

Here’s a common misconception around owner salary:

That “salary needed” figure is your personal income requirement, used by lenders to calculate whether the deal generates enough cash flow to cover both the business’s debt service and your personal living expenses.

🔍 Pro tip: “Salary needed” isn’t what you want — it’s what you require to survive. Overstating it just reduces your debt capacity and worsens your loan terms.

Now the good news...

FIXING THE DEAL

4 Tweaks That Made the Math Work

The Contrarian Community helped Kurt implement 4 tweaks to the deal structure:

Reduce purchase price to $1.5M

Extend seller note to 10 years

Reduced his “salary needed” from $100k to $75k

Set the superstar’s comp at a more realistic $75k

The Potential Results:

Debt service coverage: 1.39x → 1.48x (much safer for bank approval)

Annual savings: ~$24k in debt service payments

Purchase price: $250k reduction

Employee retention: Realistic comp plan keeps key people

Kurt Could Potentially Save $250k and Gain $24k Annual Cash Flow

Kurt came in confident. He left educated. Hants’ final verdict?

"A major hurdle still to cross is the working capital evaluation," Kurt told us.

Kurt is now building a comprehensive financial model based on actual job data, working closely with the broker to understand the business's complex working capital dynamics.

The deal is still in the air.

Want your deal reviewed by hundreds of smart business builders and buyers?

Get access to our real-time deal review sessions when you join the Contrarian Community.

The information contained here is educational, may not be typical, and does not guarantee returns. Background, education, effort, and application will affect your experience and the profitability of any business. Individual results may vary.

.avif)

%20(3).png)

.png)

%20(1).png)

.png)

.svg)