You're not stuck, you're just alone at the top. Most entrepreneurs hit a ceiling, not because the opportunity isn't there, but because you're solving $10M problems with $1M strategies.

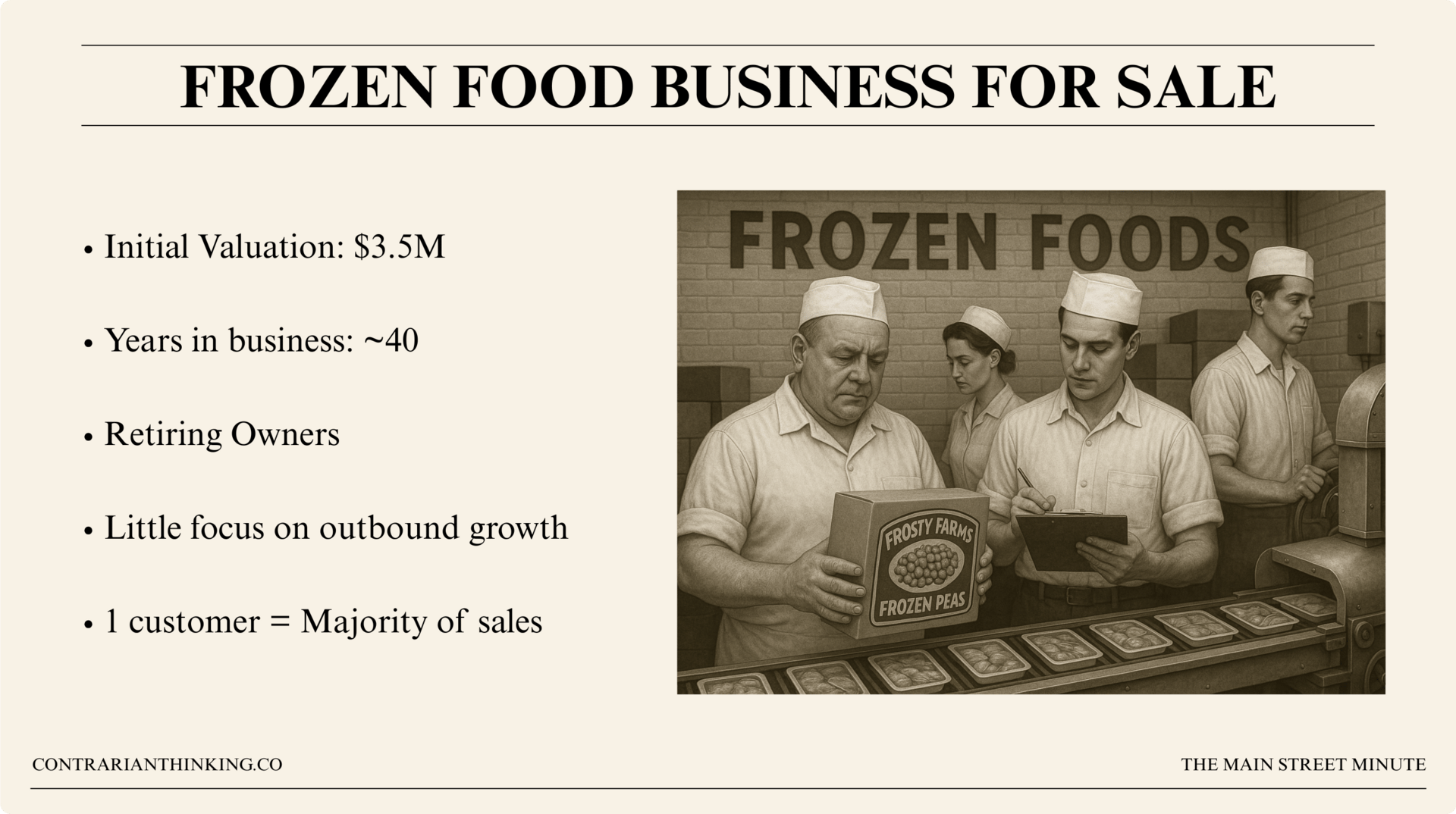

Today’s deal is a relationship-driven B2B frozen food wholesaler built by a husband-and-wife team. It’s lean, profitable, and surprisingly simple: no employees (really), no inventory, and just a handful of key players holding it all together.

For Mark, the buyer, it checked a lot of boxes.

The business has strong cash flow. It’s been remarkably consistent. And after nearly four decades of running it quietly and efficiently, the soon-to-retire owners, now in their late 70s, are finally ready to pass the torch.

But beneath that calm surface is a single relationship that’s carried the business for decades: one customer that makes up nearly 70% of revenue.

That could be a sign of durability… or a disaster waiting to happen.

Let’s take a look under the hood.

DEAL GLANCE

What It Has Going For It

This business was built to be lean. No inventory. No employees. No overhead bloat. Just co-packers making the food and brokers getting it sold.

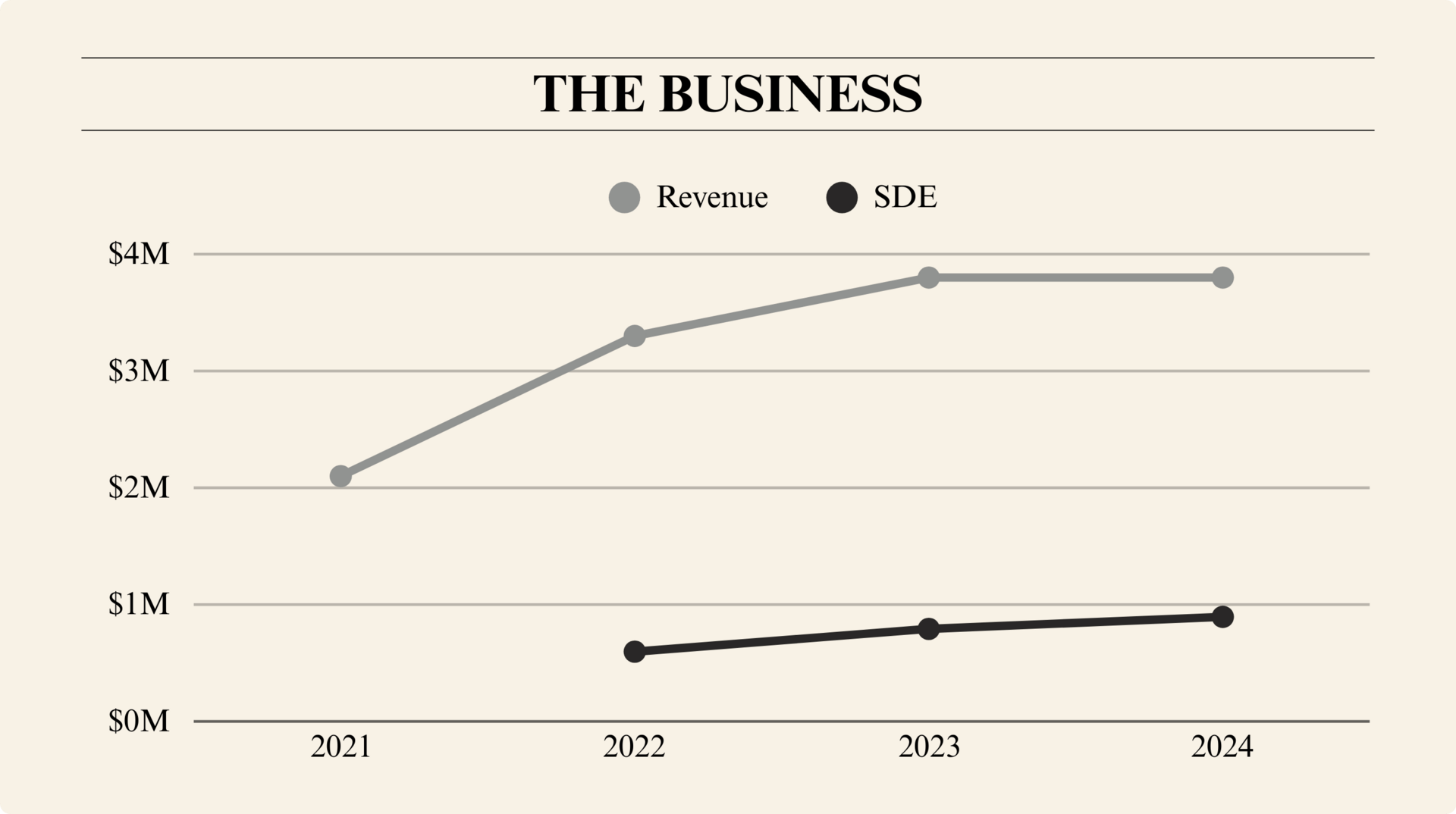

According to Mark, the sellers even “intentionally avoided growth to keep operations small and manageable.” And yet, the business has grown anyway.

In late 2024, a major new customer came on board — and it’s already moving the needle. Mark believes this buyer will become the company’s second-largest customer, reducing concentration from ~70% to ~58% by the end of this year.

It’s a business built on relationships, and Mark sees that as a feature, not a bug.

He and his business partner come with deep expertise and networks in hospitality. They’ve both run operationally complex companies and aren’t concerned about learning the nuances of this one.

Their plan is also to go where the seller never did: outbound.

They’re planning to grow by leaning into their networks: hotel chains, cruise lines, and large foodservice contracts. The current owners spend maybe 10%-15% of their time on sales. Mark will be doing closer to 100% on Day 1.

DIGGING DEEPER

Industry Snapshot

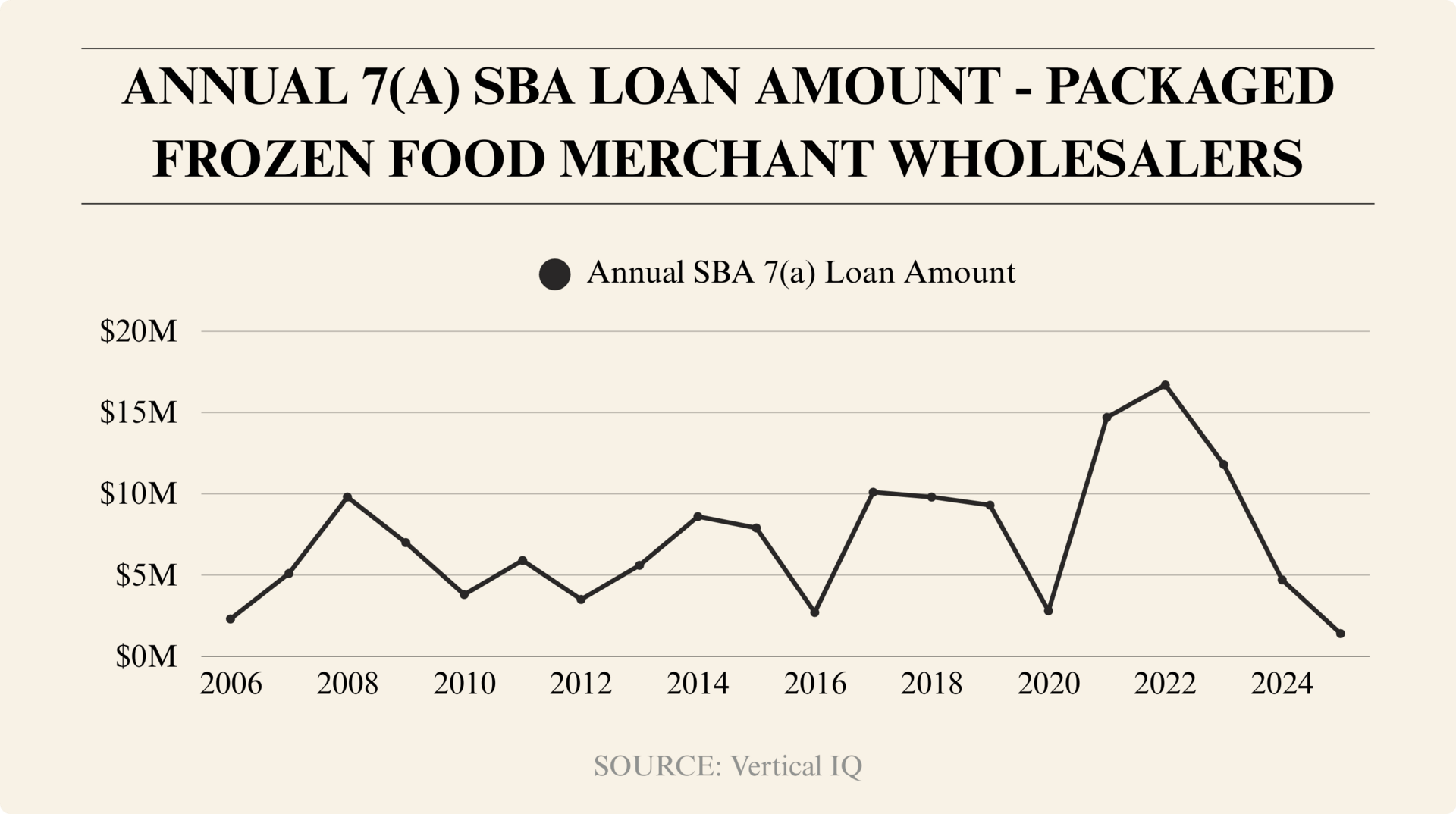

Frozen food wholesaling is a $151B market, and most of it is dominated by big players moving generic products at scale.

This business is focused on private-label goods like egg rolls and spring rolls sold into hot bars, cruise ships, and buffets. No inventory. No real brand. Just a product that reheats well and relationships that have lasted decades.

That’s the upside: lean ops, consistent margins, high repeat volume.

The downside? The model is hard to value and hard to underwrite, especially without many contracts or hard assets to back it up. (You’re buying trust, not trucks.)

SBA lending to food distribution has fallen in the past few years. Low SBA lending to frozen food wholesalers could signal that these businesses are asset-light, relationship-heavy, and riskier to underwrite, meaning buyers need strong operational chops and creative deal structures to succeed.

Still, for the right buyer with foodservice connections and an appetite for relationship-driven growth, it’s a wedge into a giant industry.

COMPS

What’s It Worth?

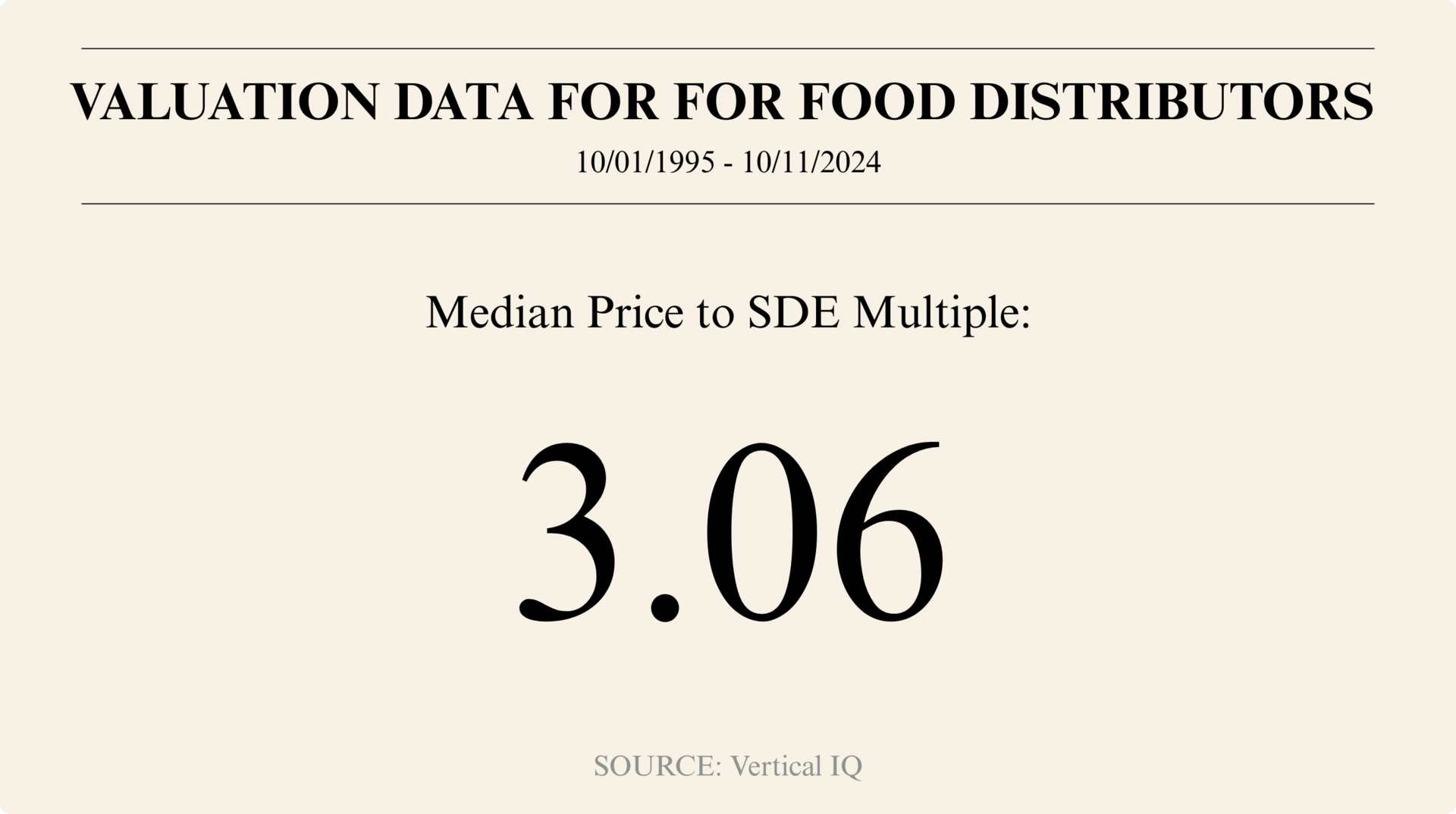

This deal is priced at just under 4x 2024 SDE.

Mark’s proposed financing:

10% down payment

75% SBA loan

15% seller financing

But this isn’t a typical business with assets, contracts, or staff. It’s lean and fragile.

Here’s what you’re getting:

No employees

No ops team to retain

No hard assets

Few long-term agreements

A single customer driving ~70% of revenue

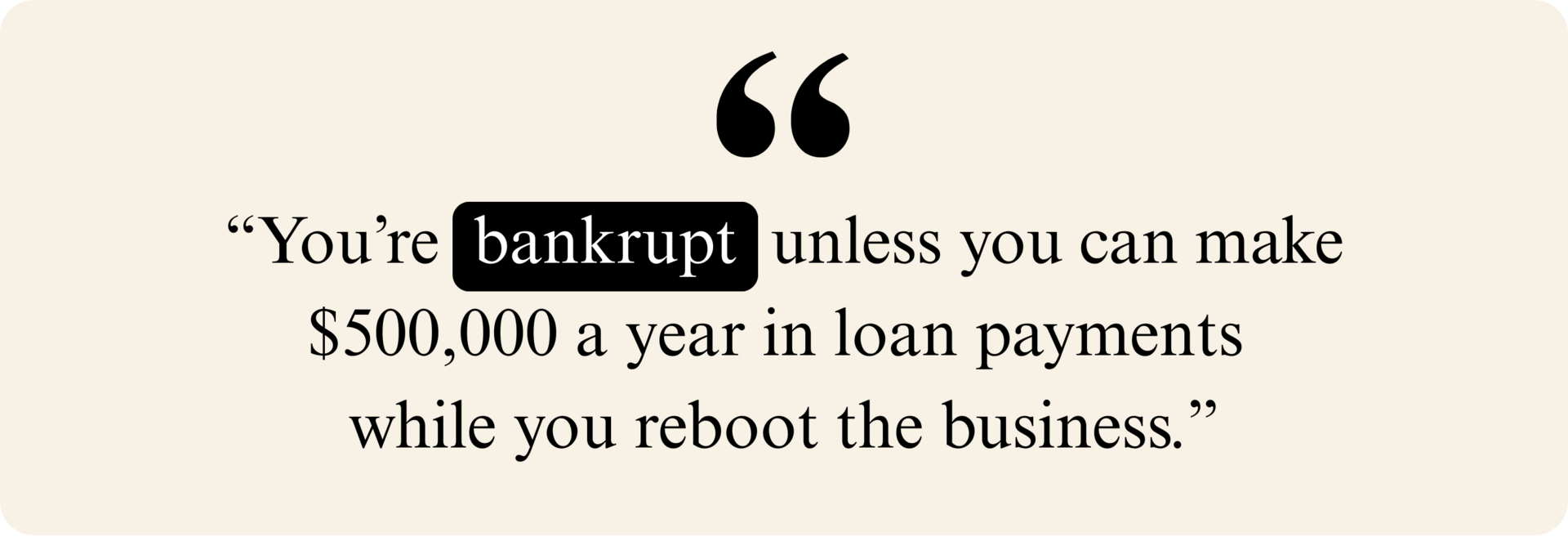

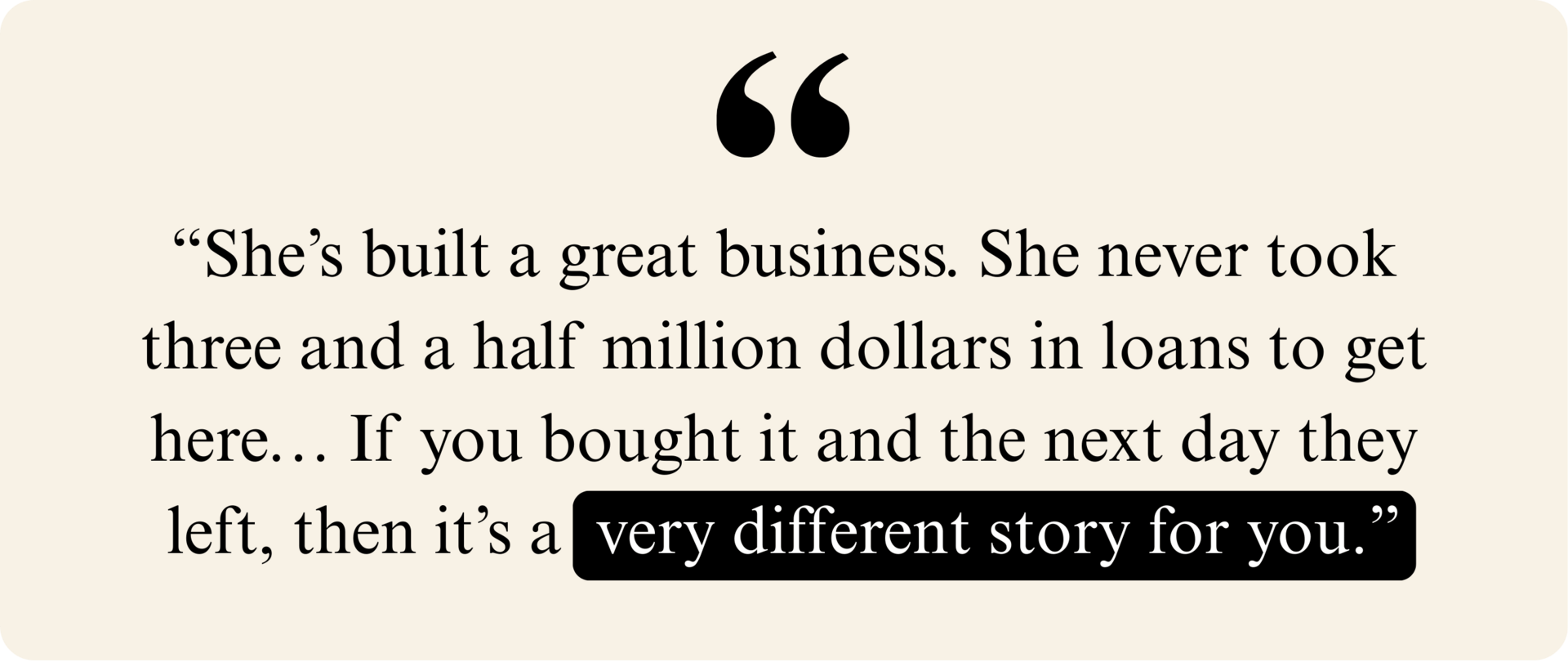

As one community member put it, “If that customer leaves and you’ve got a $3.5M loan and zero infrastructure…”

So, how does the valuation stack up?

Let’s look at where food distributors typically land on multiples, keeping in mind this is a related but not identical business model:

All this is why the parties are negotiating on a creative safety net: a $500k+ seller note that gets forgiven over time if the biggest customer starts to shrink.

Here’s how it works:

If Customer #1 falls below 50% of total revenue, the note is forgiven in 20% chunks per year over five years

If they don’t? The full balance comes due in a balloon payment in 2029

It’s a smart buffer, but not a full parachute. If that customer churns, the seller note helps, but you’re still on the hook for hundreds of thousands in annual SBA payments while rebuilding the top line.

RED FLAGS

1 Big Potential Roadblock

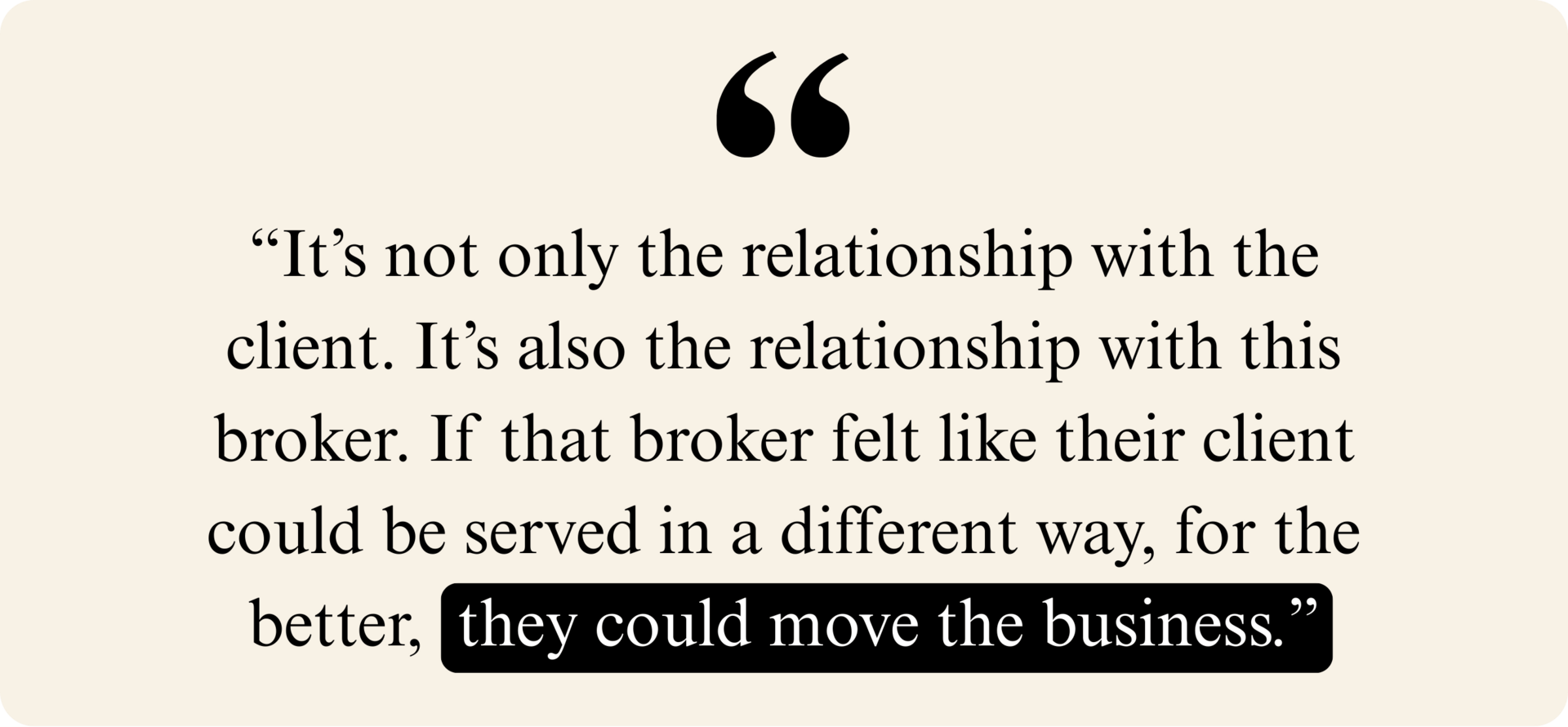

This business doesn’t just rely on one major customer: it depends on someone else’s relationship with that customer.

Here’s how it works: Customer #1 accounts for nearly 70% of total revenue. But the seller doesn’t interact with them directly. That relationship is managed by a third-party food broker.

That dynamic raised immediate red flags during the community review, including from one of our deal coaches, Candice:

In other words, the customer doesn’t just have the power to leave: the broker could take them elsewhere.

To mitigate that, Mark floated the idea of bringing the broker into a performance-based comp plan, not equity, but a way to keep them aligned financially. Whether the broker is open to that remains to be seen.

For now, Mark hasn’t met them. That’s scheduled for diligence.

The lesson here: if the core revenue of a business is routed through someone outside the deal, you need to know exactly what makes them stay… And what might make them leave.

THE BOTTOM LINE

What Other Experts Flagged

Our deal coaches raised additional concerns that go beyond the obvious risks:

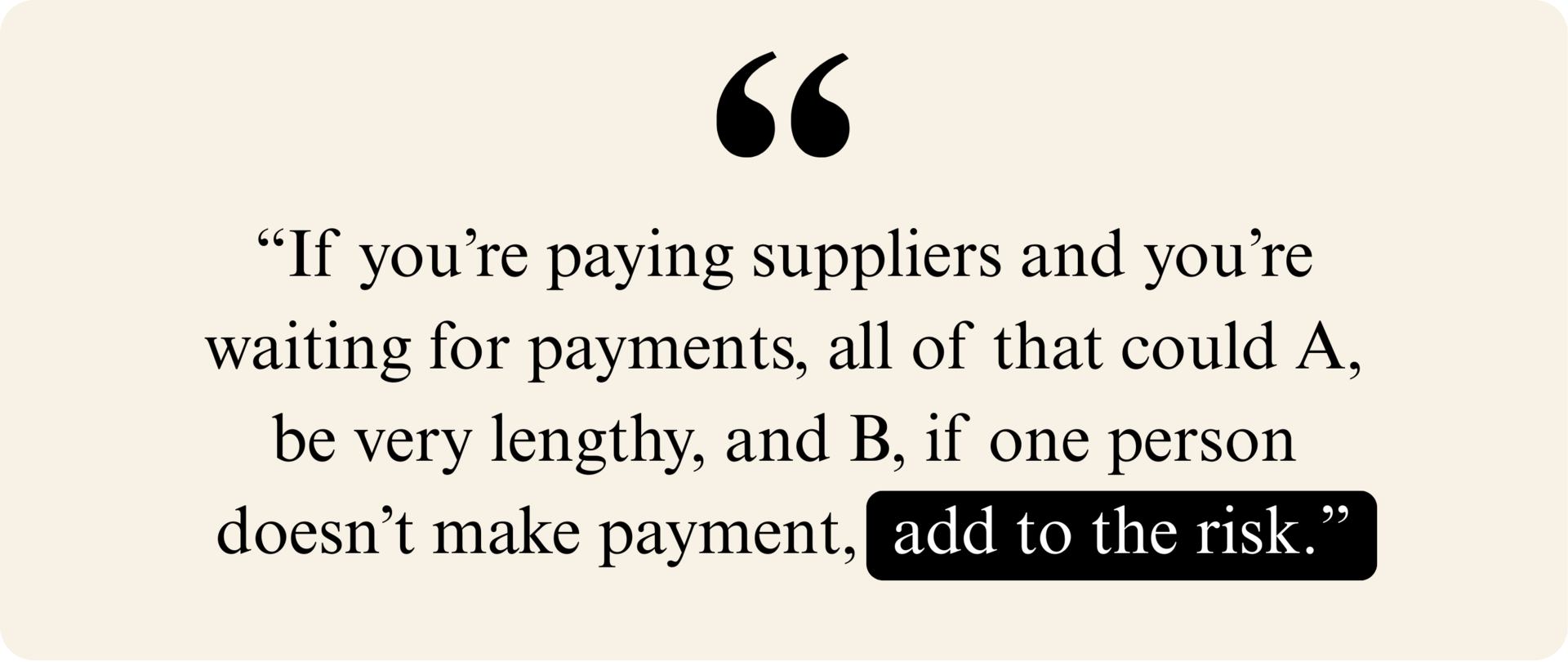

1. Cash Flow Can Compound Risk, Fast

Deal coach Candice flagged the importance of understanding the business’s cash cycle, especially when supplier payments and customer collections are mismatched.

Mark acknowledged this and confirmed the business operates on net-30 terms, offers a 1% discount for early payment, and carries no inventory. Still, with one customer making up most of the top line, any delay has an outsized impact.

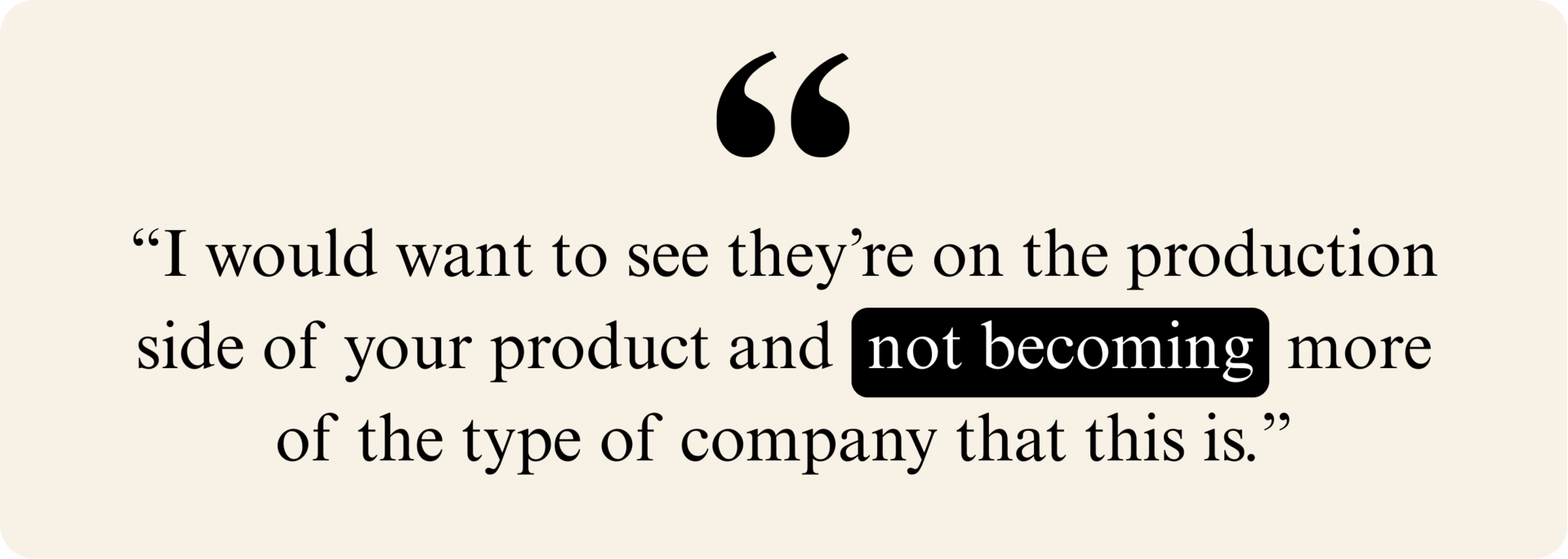

2. You Could Buy This… But Should You?

As one deal coach put it:

The seller grew this over decades, organically, likely without debt, and with minimal overhead.

Mark, on the other hand, is stepping in with a multi-million-dollar leveraged buyout. And here’s the tough question: with his industry connections, sales experience, and access to co-packers… could he build the same thing from scratch for less?

This deal isn’t just a handoff, it’s a shortcut. But shortcuts come at a premium, and with a clock attached. That doesn’t mean it’s a bad deal, just a different risk profile, and it’s important to recognize.

3. Suppliers Today, Competitors Tomorrow?

While many focused on the customer side, deal coach Stan raised a less obvious concern: supplier risk.

In plain terms: Could your co-packers go direct?

Mark mentioned that one co-packer actually introduced a new customer, a good sign. But the business is entirely reliant on two producers, and there’s still diligence to do on exclusivity and long-term alignment.

THE BOTTOM LINE

How It Played Out

At the time of the call, Mark is one of the deal’s finalists.

The seller likes him, maybe because he’s local, maybe because he’s asking the right questions.

His next steps are clear:

Meet the food broker

Review contracts

Pressure-test co-packer relationships

Find alternative financing beyond the SBA loan

Mark’s doing what real buyers do, testing the risk, not ignoring it.

The deal’s not done. But it’s in motion. And this — the messy, high-stakes middle — is where real deals get made.

The information contained here is educational, may not be typical, and does not guarantee returns. Background, education, effort, and application will affect your experience and the profitability of any business. Individual results may vary.

.avif)

%20(3).png)

.png)

%20(1).png)

.png)

.svg)