You're not stuck, you're just alone at the top. Most entrepreneurs hit a ceiling, not because the opportunity isn't there, but because you're solving $10M problems with $1M strategies.

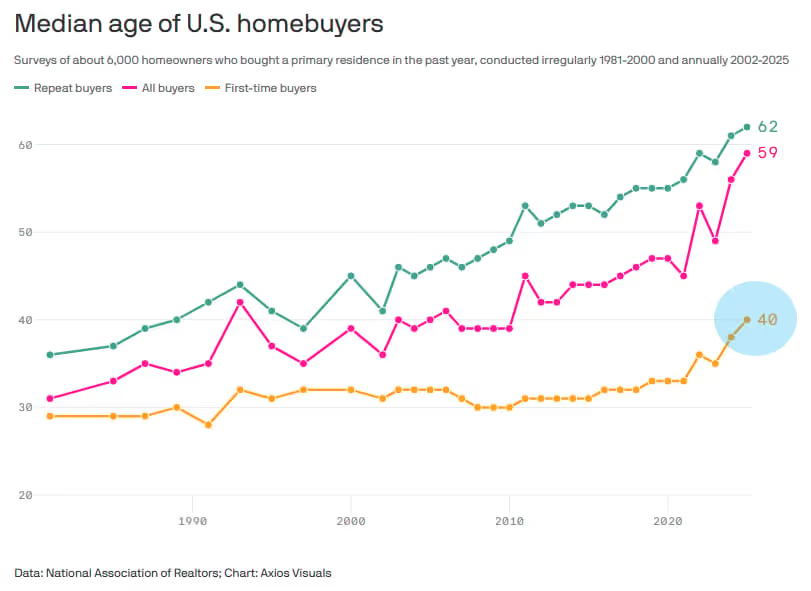

If you want to understand the next decade of politics, economics, and culture wars, start with this chart:

Young people are being locked out of homeownership. What feels like prosperity for one generation feels like punishment for the other.

How did we get here? Can we fix this? Is buying a house still a move? And if not, what can you do instead to build wealth?

How Did We Get Here?

Younger buyers aren’t imagining today’s squeeze.

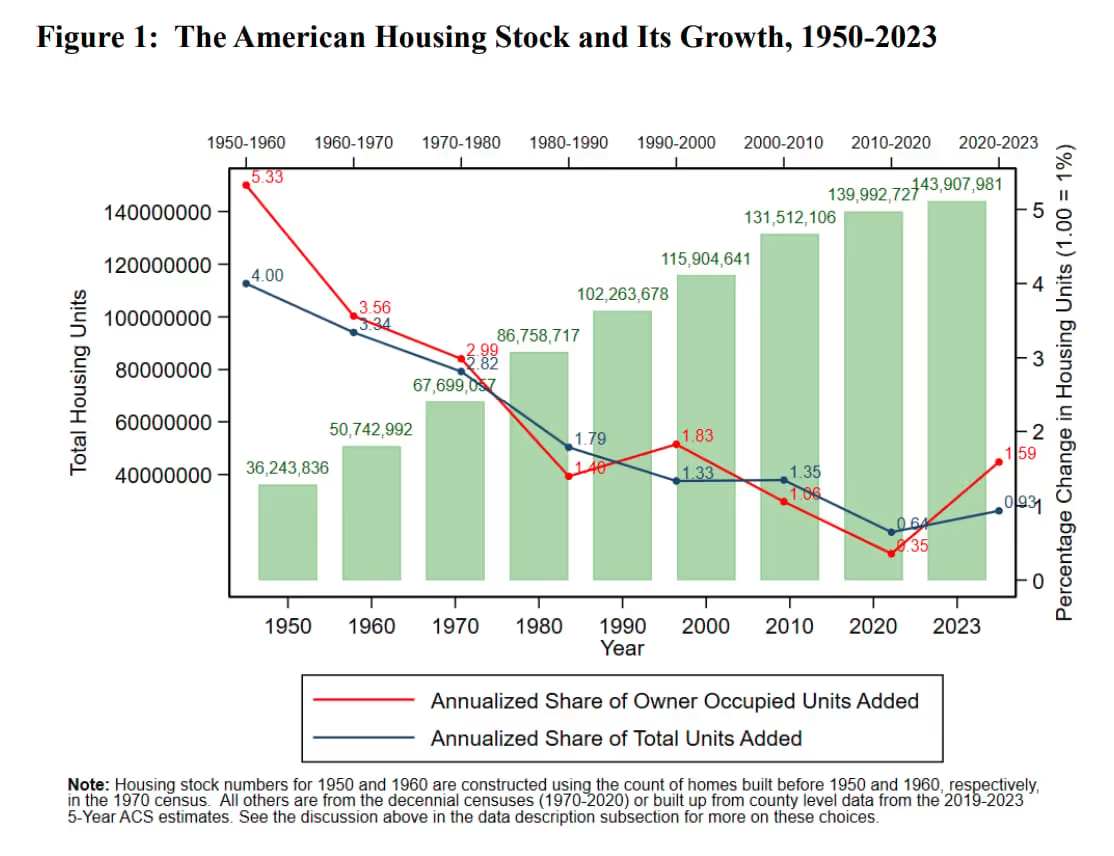

About 75 years ago, we saw one of the closest things the US has ever had to a true housing assembly line.

“The 1950s and 1960s were a golden age of new construction,” the economists Edward Glaeser and Joseph Gyourko wrote. But then things changed.

City planners began to enact zoning restrictions that limited housing construction. By the 1990s, “the growth rate of housing was barely half the rates seen in the 1950s and 1960s.”

Then, other problems arose.

The Great Recession wiped out ~40% of construction jobs by 2010. The 2010s then became the weakest US homebuilding decade per capita on record.

By the time builders recovered, millennials hit peak buying age. Their incomes were relatively higher than previous generations, but the inventory and building capacity simply weren’t there.

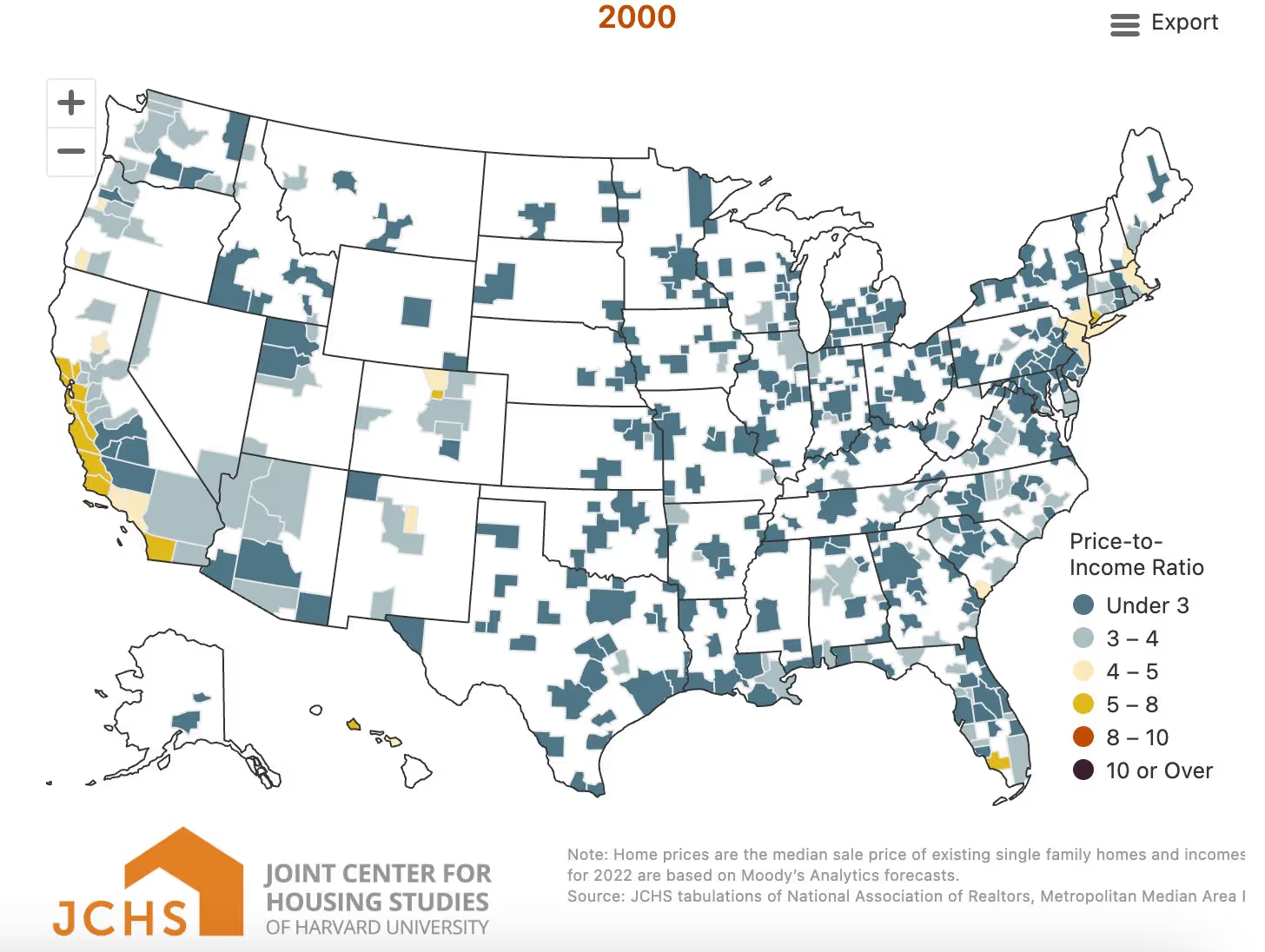

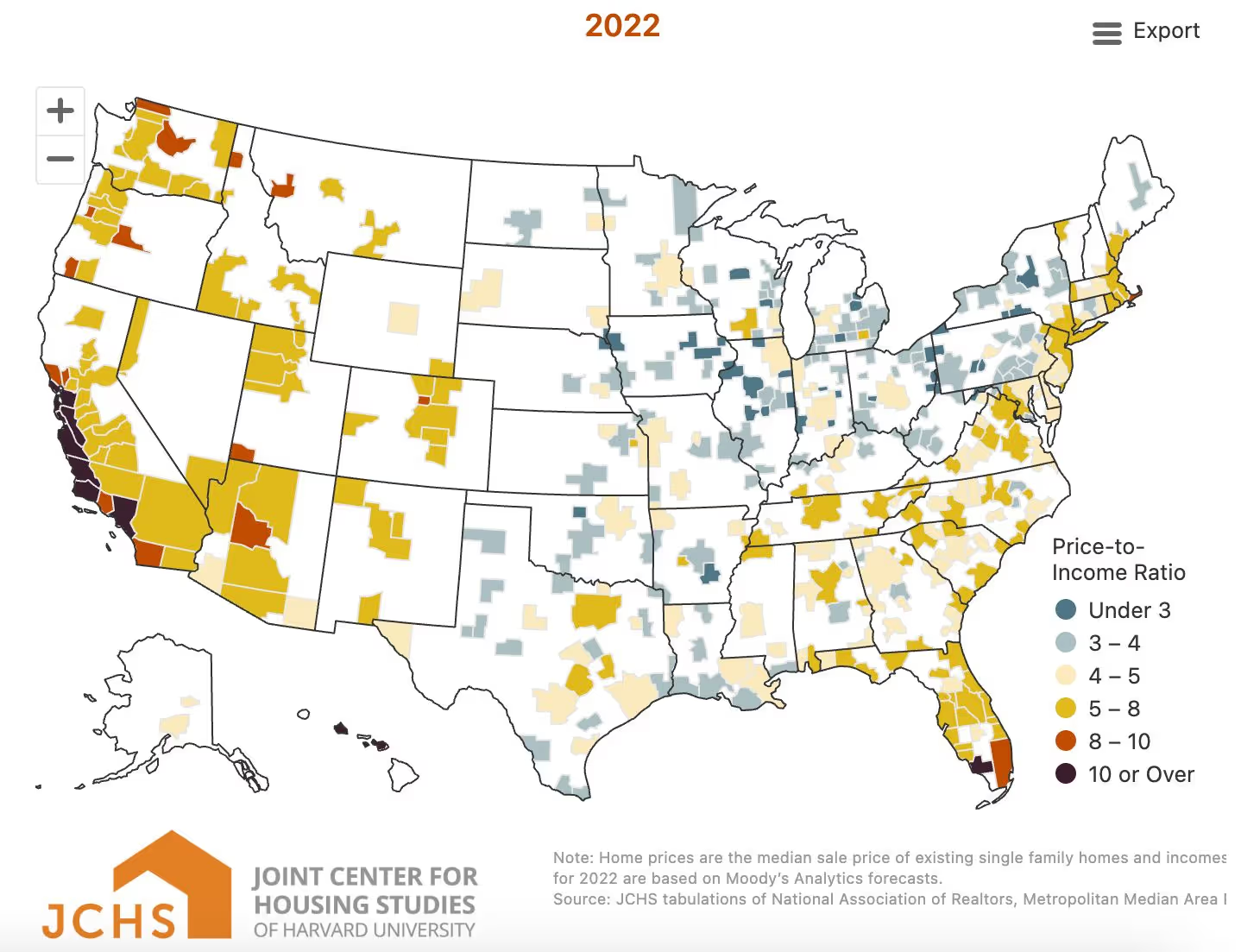

Harvard’s housing maps tell the story at a glance.

Around 2000, many markets sat near a housing price-to-income ratio of 3-to-1. Two decades later, 6 or 7-to-1 or greater became common. (Yes, 6-7 😉).

Then came the pandemic, and the market went vertical.

Demand surged. Supply chains jammed. Basic economics meant no end in sight.

When inflation followed, the pressure built up more. Mortgage rates climbed to around 7% by 2023. That spike did two things at once: it made new home purchases harder, and it froze existing owners in place.

On top of this, insurance costs and property taxes are up, meaning the all-in cost of ownership has moved higher across the board. Mix it all together, and what do you get: home sales at a 30-year low.

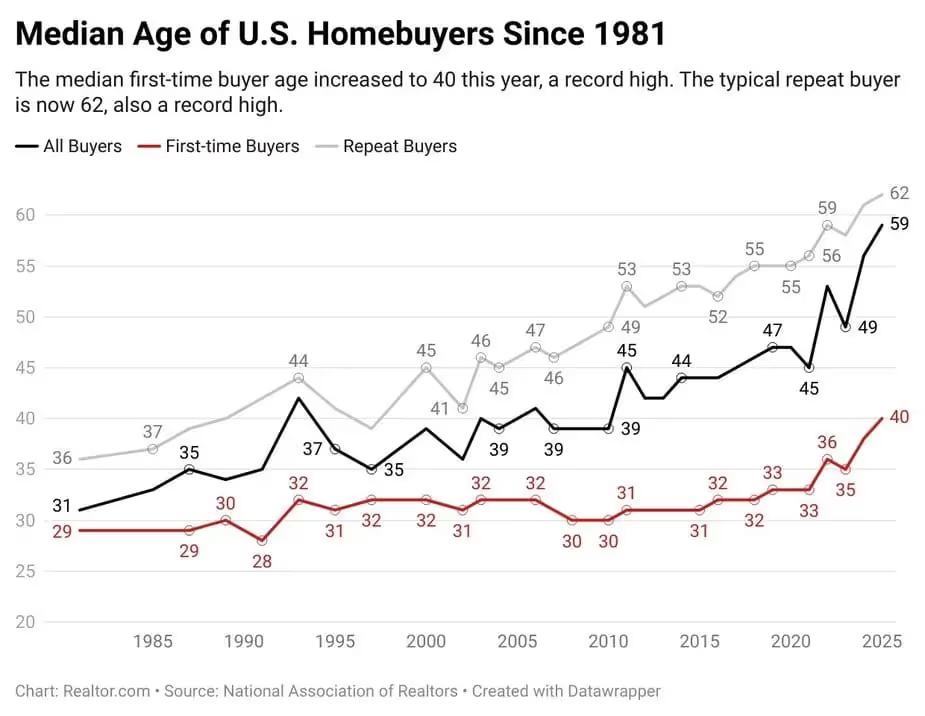

It also means you have a country where the median age of a first-time homebuyer has accelerated to 40, up from 28 in the 1990s and 30 in 2010.

Unless you’re an owner, this is not fun.

People want to imagine a future with a home, a partner, and a family. It’s no mystery why marriage, birth, and fertility rates are falling as housing slips out of reach.

When people own a house, they suddenly have a long-term reason to care about:

school systems

roads

local parks

neighborhood safety

Ownership builds belonging, pride, and civic engagement. When younger people feel like their only option is “disengaging” or “burning it all down,” unattainable housing prospects may be one reason why.

Median Age of All U.S. Home Buyers: 59-Years-Old. @CodieSanchezCT & Smerconish discuss on @CNN

Somewhere along the way, we tasked our housing system with 2 extremely important, but potentially conflicting roles: providing roofs over our heads and powerful investment vehicles. But we can’t always have our cake and eat it too…

We need to find a balance, and there’s 1 place that’s truly making it happen.

How Do You Lower Costs? 2 Words.

You build.

Seriously, it’s that straightforward.

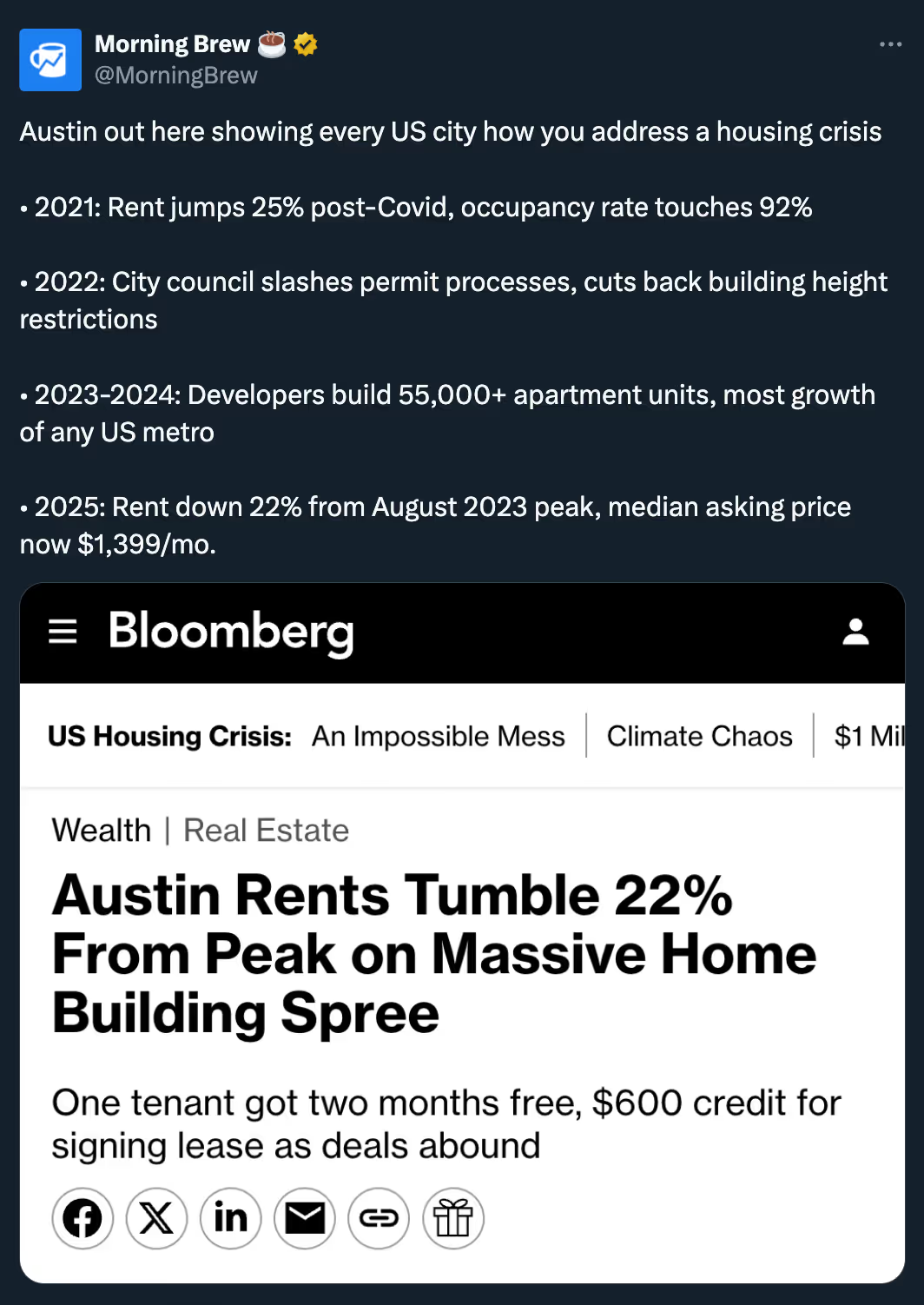

And right now, there’s no better place to look than to Austin, Texas, to see this economic theory being put into practice.

The city is one of the fastest-growing in the country. And yet, the cost to live there is… falling.

Read that again.

Demand is hot. Last decade, the city grew faster than virtually any other in the US. For a while, housing costs spiked dramatically, especially during the pandemic. It was actually quite bad.

But the city decided to do something about it, removing red tape and empowering homebuilders to build, build, and build.

By 2024, Austin was adding homes at a lightning pace, roughly 9 times faster than cities like San Francisco and LA. Pretty cool, right?

(Btw, we’re hiring in Austin, with over a dozen full-time openings in operations, strategy, and creative roles. You can view our careers page here.)

But is Buying a House Still the Goal?

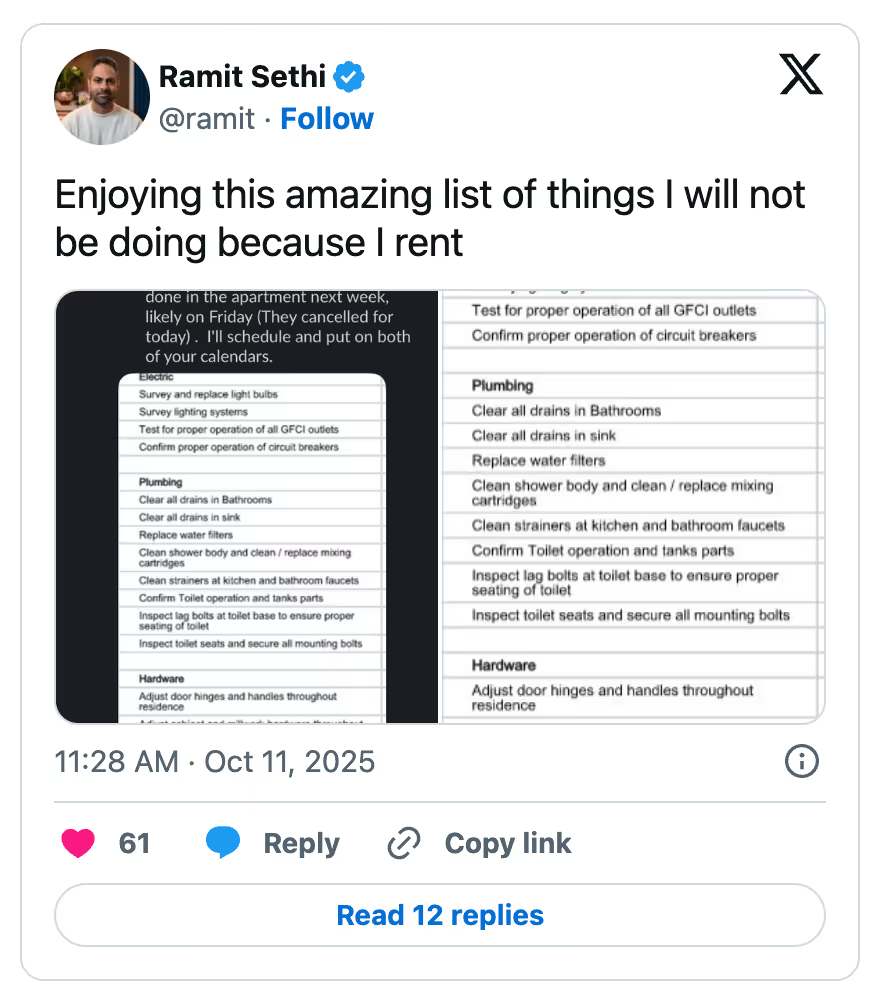

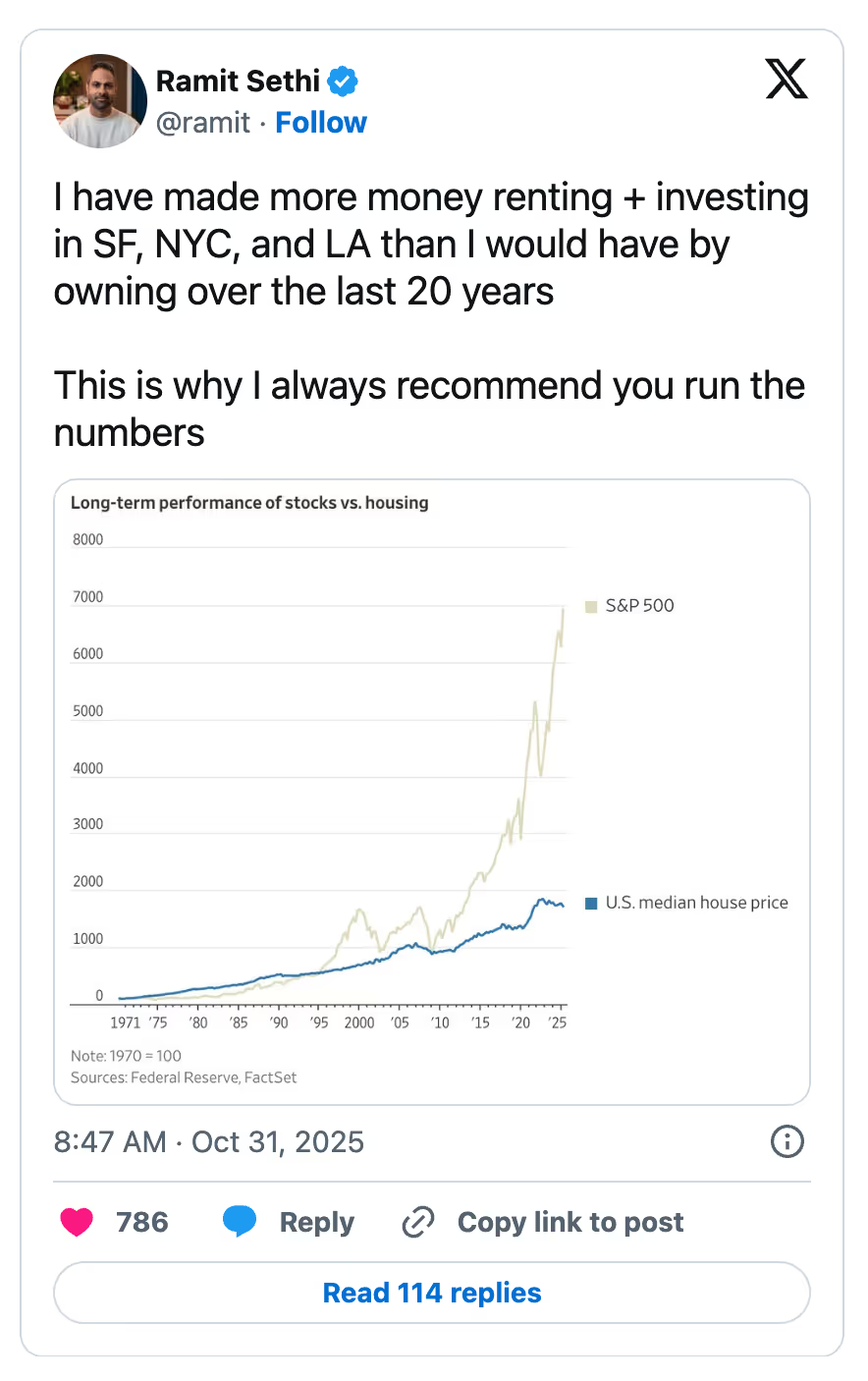

And if not, what can you do instead to build wealth? Consider these perspectives from Ramit Sethi…

Ramit is an entrepreneur, bestselling author, and personal finance expert best known for his book I Will Teach You to Be Rich, which became a huge hit for its practical, psychology-driven approach to money.

Here’s what he’ll tell you: always run the numbers. As he puts it:

Ramit makes a lot of other interesting arguments for renting > buying, including the idea that your money may be better spent renting and investing in other assets.

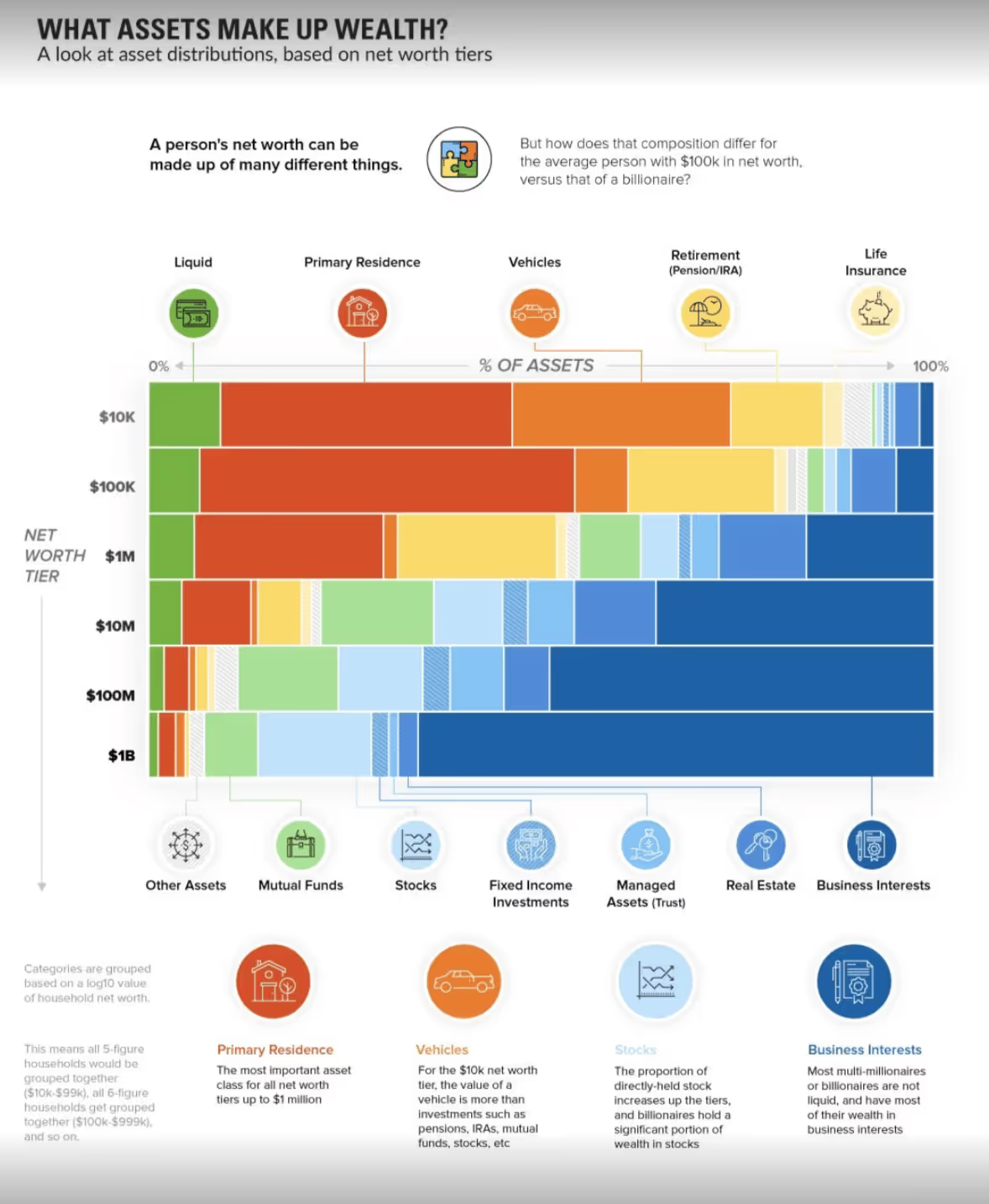

And he makes a very interesting point. If you look at what truly drives net worth beyond $1M, it is not a house. It’s business ownership stakes.

The Path We Expect More People to Take

We certainly don’t expect the younger generations to stop chasing ownership. But they may decide to change what they try to own first.

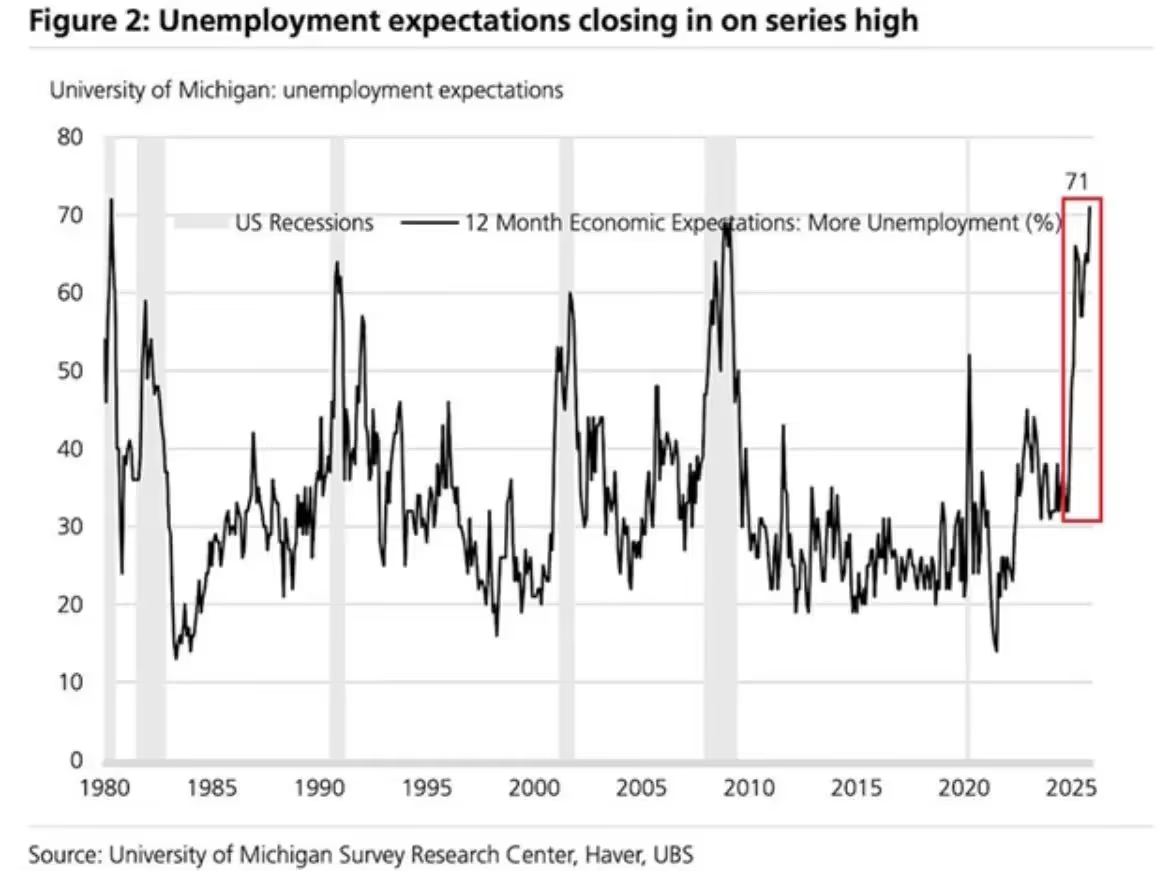

Remember, the labor market is facing a highly uncertain era.

The unemployment rate among 20-24 year olds just hit a 10-year high. More Americans were laid off in October than in any other October in ~20 years.

And people increasingly feel that unemployment is… an expectation.

Taking both the housing issues and the labor markets into account, here’s 1 life path we expect more young people will take in the coming years:

Instead of contorting themselves into a mortgage they can’t truly afford, they will rent and maintain flexibility.

They’ll focus on building income, maybe even getting married, and working to build ownership in a business rather than a home.

A business will give them things a house likely won’t: cash flow, skills, and potential job protection in a terrible labor market.

Because they’re renting, they also won’t have to worry about all the added costs and responsibilities that come with homeownership.

For years, they will focus on pouring their energy into growing sales, improving operations, and paying down acquisition debt with profits.

Any surplus cash flow can be saved or reinvested in their business, rather than into a home’s surprise roof leaks, insurance spikes, and constant maintenance.

Then, when the timing is right, they can choose to buy a home from a position of strength.

By that point, they may own a business with meaningful cash flow (potentially worth multiples more as a result of their work), along with valuable experience.

If the old path was to buy a house then build wealth, the new path might actually be the opposite: build wealth, then choose to buy a house if it makes sense for you.

But that’s just 1 perspective. Let us know what YOU think.

-Team Contrarian

ONE LAST THING…

If today’s newsletter resonated with you, these are great ways to learn even more about how to take real action:

💰 Save a spot: Join Codie on December 9th @ 6pm CT for a live virtual workshop on the 10 steps to buying the right cash-flowing business for you in 2026. (Sign up here.)

📊 Get the Main Street Minute, the only free newsletter that makes you a smarter business buyer and builder every time you open it.

DOPAMINE HITS

The information contained here is educational, may not be typical, and does not guarantee returns. Background, education, effort, and application will affect your experience and the profitability of any business. Individual results may vary.

.avif)

.avif)

%20(1).png)

.svg)