You're not stuck, you're just alone at the top. Most entrepreneurs hit a ceiling, not because the opportunity isn't there, but because you're solving $10M problems with $1M strategies.

America is fighting a civil war. No one "declared" it. Few are working to end it. And the side that's winning might not even realize it's in it.

There are no clear deaths in this war. But there are casualties. Economic ones. Millions of them. The story is right there in the numbers, if you're willing to look.

But here's what makes this a war and not just an economic trend: the conditions that produced this gap didn't appear from nowhere. They’ve been voted into existence over many decades.

When you show up for elections, you show up in policy. Federal spending on elderly programs ran at roughly 6% of GDP in 1990. By 2025, it had reached over 9%. The Congressional Budget Office projects it crossing 11% within a decade.

Those programs, plus the interest on the debt they generate, are now one of the single biggest drivers of the federal deficit. This trend is now being referred to as “Total Boomer Luxury Communism.”

“The elderly are mostly out of the job market and thus need not worry about being replaced by artificial intelligence. The majority own their homes, often debt-free. Everyone worries about health costs, but the elderly have publicly funded Medicare. None of this is true for young generations,” says the Wall Street Journal.

The Social Security trust fund peaked at $2.7 trillion in 2017. It has been declining ever since and is projected to run dry around 2033. The likely fixes — higher taxes, reduced future benefits, a later retirement age — will fall on the younger generation of workers.

Causes, symptoms, and side effects

In 1960, it is estimated that over half of 30-year-olds in America were both married and owned a home. Today, that number is around 13%.

In 1960, the overwhelming majority of young homebuying couples got there on a single income. By 2024, nearly two-thirds of young married couples had two full-time incomes.

Why the difference? In 1980, American housing often had a price-to-income ratio under 3x. Today it's more like 5x to 8x.

And because home equity is still the primary way Americans build wealth, locking a generation out of ownership is not just a housing crisis. It's a retirement crisis, a family formation crisis, and the clearest front line of this war.

But it’s not the only line.

Younger generations are spending dramatically more on “the big stuff” than previous generations, without seeing their wages keep up.

That the share of 26-year-olds investing in the stock market (good) or speculative assets like Fartcoin (bad) is rising shouldn’t surprise you. Locked out of the housing ladder, they’re routing capital into markets that are still accessible to them.

FROM OUR FRIENDS AT BEEHIIV

1 thing everyone agrees on: it’s damn nice to own something.

Social media is fun and all… until they change the algo at 2pm on a random Tuesday and half your reach disappears.

Newsletters give you something social media never will: actual ownership of your audience.

We send Contrarian Thinking to 100s of thousands of people. We use (and invested in) beehiiv for 2 reasons: they’ve thought of everything, and they make our lives wayyyyy easier. It’s all the infrastructure we could ever need:

Wildly helpful analytics

A global ad network that brings sponsors to you

An actually-good newsletter and website builder (no design skills needed)

Growth tools, ridiculously good customer support, fair pricing

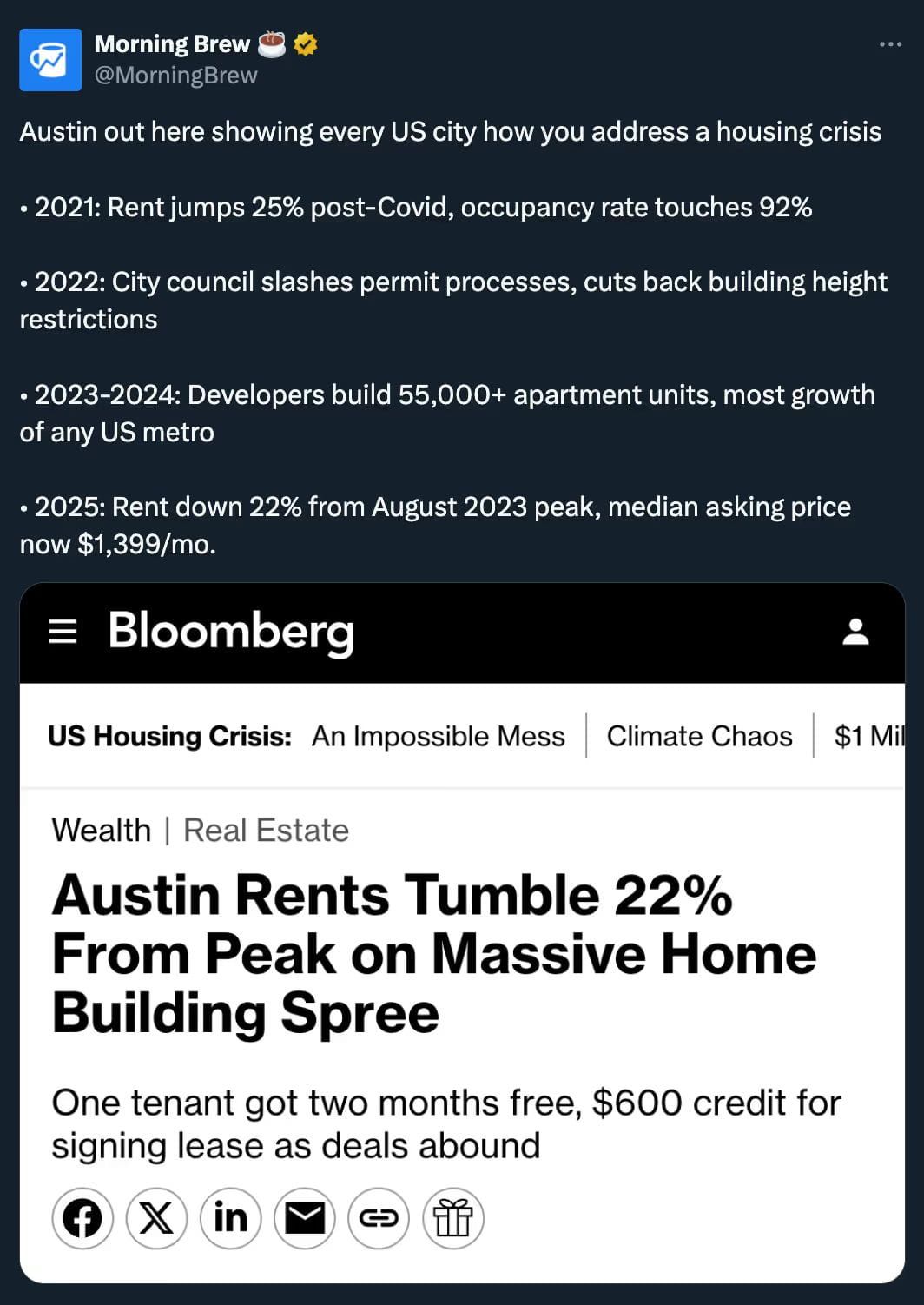

The city is one of the fastest-growing in the country. And yet, the cost to live there is… falling.

In 2024, Austin was adding homes at a lightning pace, roughly 9 times faster than cities like San Francisco and LA.

(Btw, we’re hiring in Austin, with over a dozen full-time openings in operations, strategy, and creative roles. You can view our careers page here.)

2. Next, take AI seriously as a national strategy.

AI and robotic automation may be the only realistic answer to growing productivity despite our shrinking labor pool, saving our social programs in the process.

The only way a system designed for a 4-to-1 worker-beneficiary ratio survives at a 2-to-1 rate is if each of those remaining workers produces dramatically more than their predecessors did.

That is not a conservative or liberal position. It is math. And the only credible path to that kind of productivity leap runs directly through AI and robotic automation.

Every worker who learns to wield these tools for good isn't just helping themselves. They are, quite literally, being a patriotic citizen.

Policy, education, and business investment should be oriented around deploying these tools so that benefits and wealth are felt broadly and quickly.

3. And finally… Boomers: When ready, sell your businesses to someone young and hungry.

We certainly don’t expect the younger generations to stop chasing ownership. But they may decide to change what they try to own first.

If the old path was to buy a house then build wealth, the new path might actually be the opposite: build wealth through business ownership, then choose to buy a house later if it makes sense for you.

Right now, the largest cohort of small business owners in American history is retiring.

We believe there will be a patriotic bunch who do their part by intentionally selling their business to younger, hungry Americans, passing the torch of ownership onto the next generation and preserving their own wealth in the process.

That is generational wealth at its best.

And that is how you end the war.

-Team Contrarian

The information contained here is educational, may not be typical, and does not guarantee returns. Background, education, effort, and application will affect your experience and the profitability of any business. Individual results may vary.

.png)

.png)

.jpg)

%20(1).png)

.svg)